Saving Money Is Important — But Is It Enough?

Narrated by BrahmWealth.com

By Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

Most people grow up hearing:

- Save money.

- Avoid unnecessary spending.

- Keep money safe.

- Build a savings habit.

All of these are valuable financial lessons.

However, many people eventually discover something surprising:

Saving money and building wealth are not always the same thing.

This is where financial awareness becomes important.

Many hardworking individuals:

- save regularly,

- avoid excessive spending,

- and remain financially disciplined,

yet still struggle to create significant long-term wealth.

Why?

Because money that only sits idle may not always grow fast enough to beat inflation.

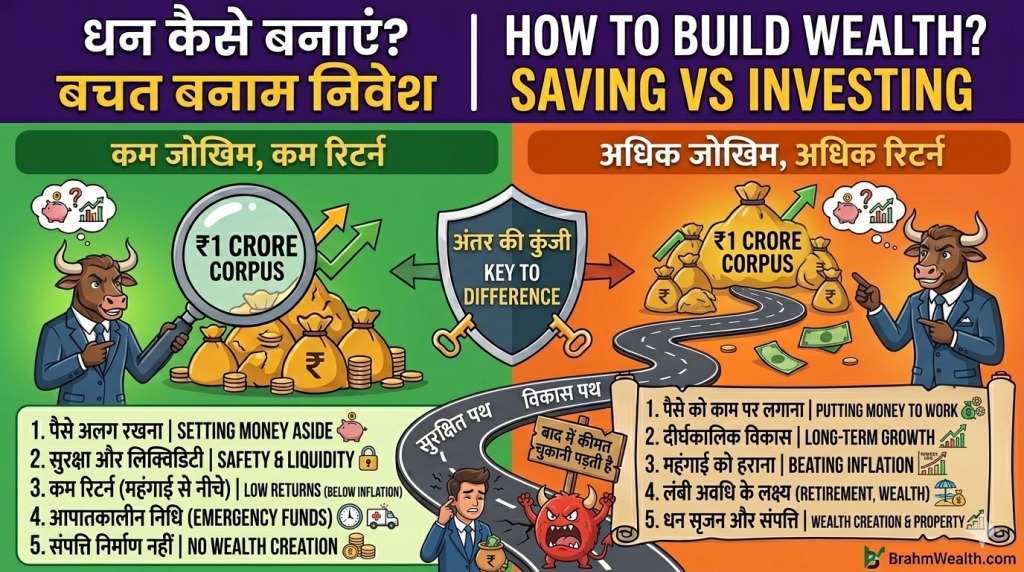

Understanding the Difference Between Saving and Investing

Saving Means

Saving generally focuses on:

- preserving money,

- maintaining liquidity,

- and handling short-term needs.

Examples:

- savings accounts,

- emergency funds,

- short-term cash reserves.

The primary objective is:

safety and accessibility.

Investing Means

Investing generally focuses on:

- growing money,

- creating long-term wealth,

- and achieving future financial goals.

Examples:

- mutual funds,

- SIP investments,

- retirement portfolios,

- long-term financial assets.

The primary objective is:

long-term growth.

Why Saving Alone May Not Be Enough

Many people assume:

“If I keep saving money consistently, I will eventually become wealthy.”

Unfortunately, inflation creates a challenge.

Over time:

- prices increase,

- purchasing power decreases,

- and future expenses become larger.

As a result:

- money that remains idle for decades may lose a significant portion of its real value.

Example 1 — The Inflation Reality

Assumptions

- Current monthly household expense = ₹40,000

- Inflation = 6%

- Time horizon = 20 years

Approximate Future Expense

| Current Expense | Future Equivalent |

|---|---|

| ₹40,000/month | ₹1.28 lakh/month |

This means:

- the same lifestyle may potentially require more than three times the money in the future.

This is why:

protecting purchasing power becomes an important financial objective.

Example 2 — Saver vs Investor

Let us compare two individuals.

Person A — Pure Saver

Assumptions

- Saves ₹10,000 every month

- Focuses only on cash accumulation

- No long-term investing habit

Result

After many years:

- money grows slowly,

- inflation continues,

- purchasing power may weaken.

Person B — Saver + Investor

Assumptions

- Maintains emergency savings

- Invests ₹10,000 monthly through SIP

- Long-term investment horizon

- Disciplined approach

Approximate Outcome After 20 Years

| Details | Amount |

|---|---|

| Total Investment | ₹24 lakh |

| Approximate Corpus | ₹95 lakh – ₹1 crore |

This demonstrates:

disciplined investing may potentially create significantly stronger long-term wealth outcomes than saving alone.

Why Financially Smart People Do Both

One common misconception is:

“Either save or invest.”

In reality:

Financially aware individuals usually do both.

Savings help with:

- emergencies,

- liquidity,

- short-term goals.

Investments help with:

- wealth creation,

- retirement planning,

- future financial freedom.

The goal is balance.

Why Emergency Funds Come First

Before aggressive investing:

many experts recommend creating:

- emergency savings,

- basic financial protection,

- and expense stability.

This may help investors:

- avoid panic,

- continue SIPs,

- and remain invested during difficult periods.

At BrahmWealth.com, financial awareness begins with building a strong foundation before focusing on wealth creation.

The Power of Long-Term Investing

Long-term investing benefits from:

- discipline,

- patience,

- consistency,

- and compounding.

For lump-sum growth awareness, the future value concept is often explained as:

FV = PV × (1 + r)^nWhere:

- FV = Future Value

- PV = Present Value

- r = Annual Return

- n = Number of Years

This formula helps estimate how money may potentially grow over time through compounding.

Why Many People Delay Investing

Common reasons include:

- fear of market fluctuations,

- lack of financial awareness,

- waiting for higher income,

- confusion about where to begin,

- or believing small amounts do not matter.

However:

even modest investments,

combined with time and discipline,

may potentially create meaningful future wealth.

Example 3 — Small SIP, Big Difference

Assumptions

- SIP = ₹5,000/month

- Expected return = 12%

- Investment duration = 25 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹15 lakh |

| Approximate Corpus | ₹85 lakh – ₹1 crore |

This demonstrates:

time and consistency often become more important than starting with large amounts.

Important Reality Check

All examples used in this article are educational illustrations based on assumptions.

Actual investment returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Investors should always evaluate:

- financial goals,

- risk tolerance,

- and investment suitability carefully.

Common Financial Mistakes Many People Make

Many people:

- save but never invest,

- delay investing repeatedly,

- underestimate inflation,

- or keep all money idle for long periods.

Others assume:

“I will start investing later.”

But long-term wealth creation often rewards:

- early action,

- disciplined investing,

- and patience.

How Can Someone Build a Better Financial Foundation?

Simple steps may include:

- Creating an emergency fund

- Understanding inflation

- Learning basic investing concepts

- Starting a SIP gradually

- Thinking long-term financially

Financial awareness usually develops one step at a time.

Final Thoughts

Saving money is an important financial habit.

But in today’s world:

- saving alone may not always be enough,

- inflation continues rising,

- and future goals become more expensive.

This is why:

- savings help protect stability,

- while investing may help create future wealth.

Because:

protecting money is important — but helping money grow responsibly may potentially be equally important.

A Small Positive Note from BrahmWealth

At BrahmWealth.com, our goal is to simplify financial awareness in practical and beginner-friendly language.

If you notice:

- any factual error,

- calculation issue,

- typing mistake,

- or financial concept improvement opportunity in this article,

your feedback is genuinely appreciated.

Learning together and improving together may help create a stronger financial awareness ecosystem for everyone.