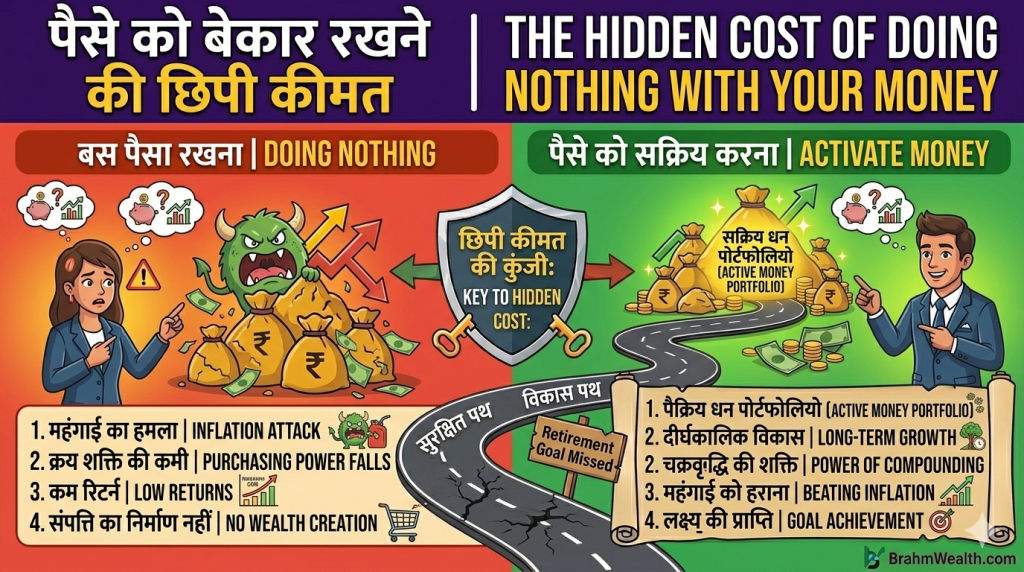

Doing Nothing May Feel Safe — But It Can Be Costly

Narrated by BrahmWealth.com

By CMA Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

When people think about financial mistakes, they often imagine:

- bad investments,

- stock market losses,

- frauds,

- or risky decisions.

However, one of the most expensive financial mistakes is often invisible.

It is:

doing nothing with your money for long periods of time.

Many people:

- keep postponing investing,

- leave large amounts idle,

- or wait endlessly for the “perfect opportunity.”

While this may feel safe,

inflation continues working silently in the background.

Over time:

- purchasing power falls,

- financial goals become more expensive,

- and wealth creation opportunities may be missed.

Why Doing Nothing Feels Comfortable

Doing nothing often feels easier because:

- there is no risk of market fluctuations,

- no need to learn investing,

- no financial decisions to make,

- and no fear of making mistakes.

This creates a false sense of security.

Because while money may appear unchanged,

its real purchasing power may gradually decline.

Understanding Opportunity Cost

One important financial concept is:

Opportunity Cost

Opportunity cost means:

the value of what you potentially miss by not taking action.

For example:

If ₹5 lakh remains idle for many years,

the loss is not only inflation.

The bigger loss may be:

- the potential growth that never happened.

Example 1 — Money Left Idle

Assumptions

- ₹5 lakh remains unused

- Time horizon = 20 years

- Inflation = 6%

What May Happen?

After 20 years:

- ₹5 lakh may still appear as ₹5 lakh,

- but its purchasing power may be significantly lower.

In practical terms:

the same money may buy much less than it does today.

Example 2 — Investing the Same Amount

Assumptions

- Lump Sum Investment = ₹5 lakh

- Expected annual return = 12%

- Investment duration = 20 years

Future Value Formula

FV = PV × (1 + r)^nWhere:

- FV = Future Value

- PV = Present Value

- r = Annual Return

- n = Number of Years

Approximate Outcome

| Details | Amount |

|---|---|

| Initial Investment | ₹5 lakh |

| Approximate Future Value | ₹48 lakh+ |

This demonstrates:

money that works may potentially create significantly different outcomes compared to money that remains idle.

Why Inflation Is the Silent Wealth Destroyer

Inflation rarely attracts attention because:

- it happens gradually,

- year after year,

- without creating immediate fear.

Yet inflation affects:

- groceries,

- healthcare,

- education,

- travel,

- housing,

- and retirement expenses.

Example 3 — Cost of Delay

Suppose:

- You plan to start investing next year.

- Then delay again.

- Then postpone once more.

After 10 years:

the missed opportunity may potentially become much larger than the amount originally invested.

This is because:

- time cannot be recovered,

- compounding cannot work retrospectively.

Why Time Is One of the Biggest Wealth Creation Factors

Most people focus on:

- investment returns,

- market conditions,

- economic news.

But one factor remains extremely powerful:

Time

The earlier money begins working,

the longer compounding has to operate.

This is why many successful long-term investors focus on:

starting rather than waiting.

Small Investments Can Matter More Than Expected

Many beginners believe:

“I need a large amount before investing.”

In reality:

even small investments,

combined with consistency and time,

may potentially create meaningful wealth.

Example 4 — ₹3,000 Monthly SIP

Assumptions

- SIP = ₹3,000/month

- Expected return = 12%

- Investment duration = 25 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹9 lakh |

| Approximate Corpus | ₹40 lakh+ |

This demonstrates:

- small beginnings,

- long-term discipline,

- and compounding

may potentially create meaningful future financial outcomes.

Correct SIP Future Value Formula

M = P × [((1 + i)^n − 1) / i] × (1 + i)Where:

- M = Future maturity value

- P = Monthly SIP amount

- i = Monthly rate of return

- n = Total number of monthly instalments

This formula helps estimate how regular monthly SIP investments may potentially grow over time through compounding and disciplined investing.

Why Financial Awareness Matters

Financial awareness is not only about:

- earning more money,

- increasing salary,

- or finding higher returns.

It is also about:

- avoiding costly delays,

- understanding inflation,

- and making money work productively.

At BrahmWealth.com, the objective is to help individuals understand these concepts through practical, beginner-friendly financial education.

Important Reality Check

All examples in this article are educational illustrations based on assumptions.

Actual investment returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Investors should evaluate:

- financial goals,

- risk tolerance,

- investment suitability,

- and time horizon carefully.

Common Financial Mistakes Many People Make

Many people:

- keep money idle for too long,

- delay investing repeatedly,

- underestimate inflation,

- or wait endlessly for the perfect opportunity.

Others believe:

“I will start next year.”

Unfortunately:

next year often becomes another year of delay.

How Can Someone Take Action Today?

Simple steps may include:

- Building emergency savings

- Understanding inflation

- Learning basic investing concepts

- Starting a manageable SIP

- Thinking long-term financially

Progress usually starts with one small step.

Final Thoughts

The biggest financial mistake is not always losing money.

Sometimes:

the biggest cost comes from money that never got the opportunity to grow.

Because:

- inflation never pauses,

- time never stops,

- and compounding rewards action more than intention.

A Small Positive Note from BrahmWealth

At BrahmWealth.com, our mission is to simplify financial awareness through practical and easy-to-understand education.

If you notice:

- any factual error,

- calculation issue,

- typing mistake,

- or concept that can be improved,

your feedback is sincerely appreciated.

Learning together and improving together may help create a stronger financial awareness ecosystem for everyone.