Retirement Is No Longer Just About “Stopping Work”

Narrated by BrahmWealth.com

By Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

Earlier, many people believed:

retirement expenses would naturally reduce with age.

But modern financial reality is changing rapidly.

Today:

- people are living longer,

- healthcare expenses are rising,

- inflation is increasing,

- and retirement periods may last 25–30 years or more.

As a result:

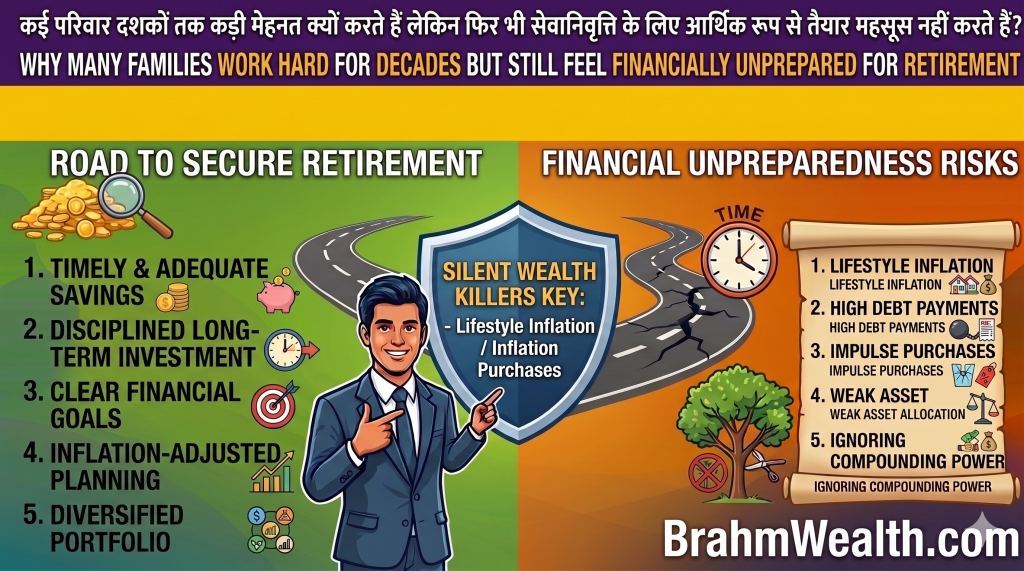

many families work hard for decades but still feel financially uncertain about retirement.

This is why retirement awareness is becoming one of the most important parts of long-term financial planning.

Why Retirement Planning Often Gets Delayed

Many people postpone retirement planning because:

- retirement feels “far away,”

- current expenses already feel high,

- or salary growth creates temporary comfort.

Some people assume:

“Future income growth will automatically solve retirement problems.”

Unfortunately:

- inflation continues,

- time passes,

- and delayed investing reduces compounding power significantly.

Example 1 — Starting Retirement Planning Early vs Late

Let’s compare two individuals.

Investor A — Starts Early

Assumptions

- Starts investing at age 25

- SIP = ₹12,000/month

- Expected annual return = 12%

- Investment duration = 35 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹50 lakh+ |

| Approximate Corpus | ₹6–7 crore |

Investor B — Starts Late

Assumptions

- Starts investing at age 40

- SIP = ₹35,000/month

- Expected annual return = 12%

- Investment duration = 20 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹84 lakh |

| Approximate Corpus | ₹3–3.5 crore |

Notice:

- Investor B invested significantly more money,

- yet Investor A may still potentially create larger retirement wealth because of longer compounding time.

This demonstrates:

time may become one of the biggest retirement planning advantages.

Why Inflation Makes Retirement Planning Difficult

One major reason retirement planning feels challenging is:

inflation.

Inflation gradually increases:

- food expenses,

- healthcare costs,

- travel costs,

- utility bills,

- and daily lifestyle expenses.

Example 2 — Retirement Expense Inflation

Assumptions

- Current monthly expense = ₹70,000

- Inflation assumption = 6%

- Retirement after = 25 years

Approximate Future Monthly Requirement

| Today’s Expense | Future Equivalent |

|---|---|

| ₹70,000/month | ₹3 lakh+/month |

This surprises many families because:

- future retirement expenses may potentially become much larger than expected.

This is why:

retirement planning is not only about saving money —

but also about protecting future purchasing power.

Why Many Families Remain Financially Dependent Even After Retirement

Without long-term planning:

- retirement savings may become insufficient,

- financial dependency may continue,

- and lifestyle flexibility may reduce.

Some retirees become dependent on:

- children,

- property sales,

- or emergency borrowing.

This is why financially aware investing habits become important much earlier in life.

At BrahmWealth.com, the goal is to help families understand retirement planning in simple practical language instead of complicated technical finance jargon.

Why SIP Investing Became Popular for Retirement Planning

SIP investing became popular because:

- investments happen systematically,

- discipline improves gradually,

- and compounding gets enough time to work.

Retirement planning especially benefits from:

- long-term investing,

- consistency,

- and Step-Up SIP growth.

Example 3 — Step-Up SIP for Retirement

Assumptions

- Starting SIP = ₹15,000/month

- SIP increases 10% yearly

- Expected annual return = 12%

- Investment duration = 30 years

Approximate Outcome

| Details | Amount |

|---|---|

| Approximate Total Investment | ₹2 crore+ |

| Approximate Corpus | ₹10–12 crore |

This demonstrates how:

- gradual SIP increases,

- long-term investing,

- and compounding

may potentially support meaningful retirement wealth creation.

Why Compounding Becomes Extremely Powerful for Retirement Goals

Compounding works best when:

- investments continue consistently,

- time horizon remains long,

- and withdrawals are avoided unnecessarily.

FV=P×r(1+r)n−1

This is why:

- early retirement planning,

- disciplined investing,

- and patience

may potentially create very large long-term financial differences.

Why Emotional Spending Often Delays Retirement Security

Many people prioritize:

- lifestyle upgrades,

- luxury spending,

- gadgets,

- vacations,

- and unnecessary EMIs

before:

- retirement investing,

- emergency planning,

- or long-term wealth creation.

This creates:

lifestyle inflation.

Over decades:

- investments may remain weaker than expenses,

which may potentially delay financial freedom significantly.

Important Reality Check

All investment examples in this article are educational illustrations based on assumptions.

Actual investment returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Retirement planning should always remain:

- flexible,

- realistic,

- and periodically reviewed.

Common Retirement Planning Mistakes Many Families Make

Many people:

- start retirement planning too late,

- underestimate inflation,

- stop SIPs emotionally,

- or depend completely on salary growth.

Others assume:

retirement planning can wait indefinitely.

But long-term financial stability often rewards:

- early awareness,

- disciplined investing,

- and long-term consistency.

How Can Someone Start Retirement Planning More Practically?

Simple starting steps may include:

- Starting SIP investments early

- Increasing SIP gradually with income growth

- Understanding inflation realistically

- Building emergency savings

- Thinking long-term financially

Retirement planning usually becomes easier when started gradually and consistently.

Final Thoughts

Retirement planning is not about fear.

It is about:

- preparing gradually,

- protecting future financial dignity,

- and reducing future financial dependency.

Because:

salary income eventually stops —

but expenses and inflation usually continue.

This is why:

- disciplined SIP investing,

- long-term compounding,

- and retirement awareness

- may potentially become extremely valuable over time.