Higher Income Does Not Always Create Financial Peace

Narrated by BrahmWealth.com

By Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

Many people assume:

“Once my salary becomes high enough, financial stress will automatically disappear.”

But reality often feels very different.

Today, many individuals:

- earn more than before,

- receive salary increments regularly,

- and continuously improve their lifestyle,

yet still feel:

- financially pressured,

- dependent on monthly income,

- or worried about future expenses.

Why does this happen?

Because:

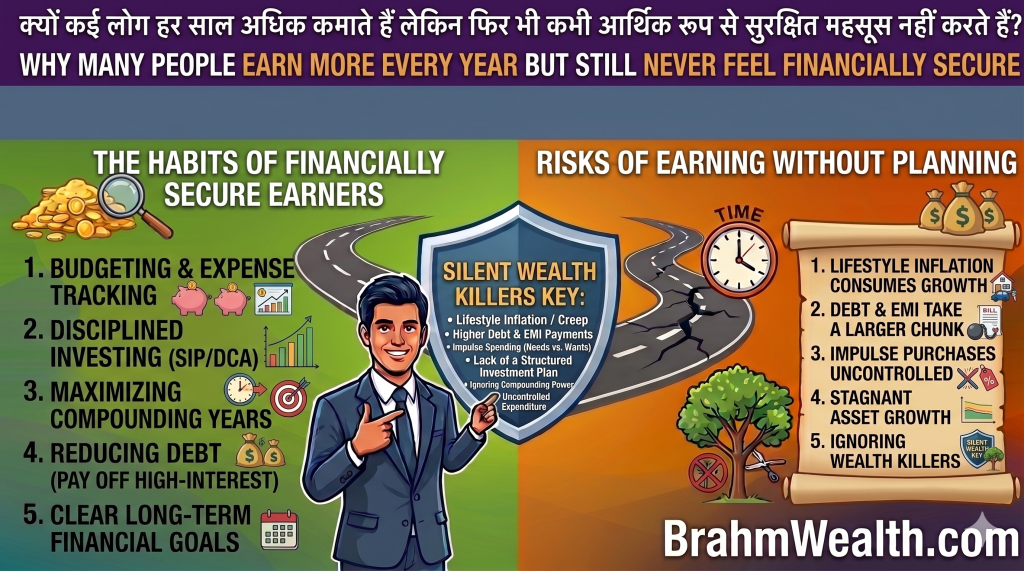

financial security usually depends not only on income —

but also on financial behavior.

This is one of the biggest financial awareness lessons many people realize very late in life.

Why Financial Stress Often Continues Despite Higher Income

As income increases:

- expenses often increase faster,

- lifestyle upgrades become normal,

- and financial expectations continue rising.

Examples include:

- bigger EMIs,

- expensive gadgets,

- luxury spending,

- subscription overload,

- frequent vacations,

- and social comparison expenses.

This is called:

lifestyle inflation.

Without disciplined investing:

- income may grow,

but: - long-term wealth may still remain limited.

Example 1 — Same Income, Different Financial Outcomes

Let’s compare two individuals.

Person A — Higher Lifestyle, Lower Investments

Assumptions

- Monthly income = ₹1.5 lakh

- Large EMIs

- Minimal SIP investing

- Lifestyle expenses rise every year

- No long-term financial planning

Possible Long-Term Result

After 20–25 years:

- limited wealth creation,

- continued salary dependency,

- and higher financial pressure.

Person B — Balanced Lifestyle + Investing Discipline

Assumptions

- Monthly income = ₹1.5 lakh

- ₹25,000 monthly SIP

- Emergency fund maintained

- Step-Up SIP increases yearly

- Controlled lifestyle inflation

Approximate Long-Term Outcome

| Details | Amount |

|---|---|

| Approximate Corpus After 25 Years | ₹4–5 crore+ |

This demonstrates:

disciplined investing behavior may potentially matter more than income growth alone over long periods.

Why Lifestyle Inflation Quietly Delays Financial Freedom

Lifestyle inflation usually happens gradually.

Initially:

- small upgrades feel harmless.

But over years:

- recurring expenses become large,

- savings reduce,

- and investment capacity weakens.

This may quietly delay:

- retirement security,

- financial freedom,

- and long-term wealth creation.

At BrahmWealth.com, the focus is not only on investing awareness — but also on understanding practical financial behavior in modern life.

Example 2 — Small Monthly Spending vs Long-Term SIP

Assumptions

- ₹20,000 monthly discretionary lifestyle spending

- Same amount invested through SIP

- Expected annual return = 12%

- Investment duration = 25 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹60 lakh |

| Approximate Corpus | ₹2–3 crore+ |

This demonstrates:

- small recurring financial decisions,

- repeated consistently over decades,

may potentially create huge long-term financial differences.

Why Financial Security Requires Asset Creation

Many people remain focused only on:

- earning money.

But financial freedom usually depends more on:

- building assets.

Assets may potentially include:

- SIP portfolios,

- retirement investments,

- long-term wealth corpus,

- emergency reserves,

- and appreciating financial assets.

Without assets:

- financial dependency on salary income often continues indefinitely.

Why SIP Investing Became Popular for Wealth Creation

SIP investing became popular because:

- investing becomes systematic,

- discipline improves gradually,

- and compounding gets enough time to work.

This helps support:

- long-term investing behavior,

- retirement planning,

- and gradual wealth creation.

Example 3 — Moderate SIP, Long-Term Wealth Difference

Assumptions

- SIP = ₹15,000/month

- Expected annual return = 12%

- Investment duration = 25 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹45 lakh |

| Approximate Corpus | ₹2.5–3 crore |

This demonstrates:

- moderate consistent investing,

- combined with long-term patience,

may potentially create meaningful future financial security.

SIP Future Value Formula

Where:

- M = Future maturity value

- P = Monthly SIP amount

- i = Monthly rate of return

- n = Total number of monthly instalments

This formula helps estimate how regular monthly SIP investments may potentially grow over time through compounding and disciplined long-term investing.

Monthly Rate Formula

i=12×100Annual Return

Total Number of Months Formula

n=Years×12

Why Many High Earners Still Feel Financially Insecure

Common reasons include:

- lack of investing discipline,

- emotional spending,

- delayed retirement planning,

- high debt dependency,

- and insufficient financial awareness.

Some people assume:

future salary growth alone will solve everything.

But long-term financial security often requires:

- asset creation,

- disciplined investing,

- and controlled lifestyle inflation.

Why Financial Awareness Is Becoming More Important Today

Modern financial life is becoming increasingly complex because:

- inflation is rising,

- retirement periods are longer,

- healthcare costs are increasing,

- and financial responsibility is growing.

This is why:

- long-term investing awareness,

- SIP discipline,

- and financial education

may potentially become extremely valuable in modern life.

Important Reality Check

All investment examples in this article are educational illustrations based on assumptions.

Actual returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Investors should always evaluate:

- financial goals,

- risk tolerance,

- and suitability carefully.

Common Financial Mistakes Many People Make

Many people:

- increase expenses faster than investments,

- delay investing repeatedly,

- depend completely on salary income,

- or underestimate inflation.

Others assume:

financial planning can begin later.

But long-term wealth creation often rewards:

- consistency,

- patience,

- and disciplined financial behavior.

How Can Someone Improve Financial Security Practically?

Simple starting steps may include:

- Starting SIP investments early

- Increasing SIP gradually with income growth

- Controlling unnecessary lifestyle inflation

- Building emergency savings

- Thinking long-term financially

Financial awareness usually improves step by step over time.

Final Thoughts

Higher income is important.

But long-term financial security often depends more on:

- disciplined investing,

- controlled financial behavior,

- and gradual asset creation.

Because:

earning more money may improve lifestyle —

but building long-term assets may potentially improve future financial freedom.

A Small Positive Note from BrahmWealth

At BrahmWealth.com, our goal is to simplify financial awareness in practical and beginner-friendly language.

If you notice:

- any factual error,

- calculation issue,

- typing mistake,

- or financial concept improvement opportunity in this article,

your feedback is genuinely appreciated.

Learning and improving together may help create a stronger financial awareness ecosystem for everyone.