One of the Most Common Financial Mistakes Is Waiting Too Long to Start

Narrated by BrahmWealth.com

By Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

Many people want to begin investing.

But they often say:

- “Markets are too high right now.”

- “I’ll start after my salary increases.”

- “I’ll begin when things become more stable.”

- “This is not the right time.”

As a result:

- months pass,

- years pass,

- and investing keeps getting delayed.

Unfortunately:

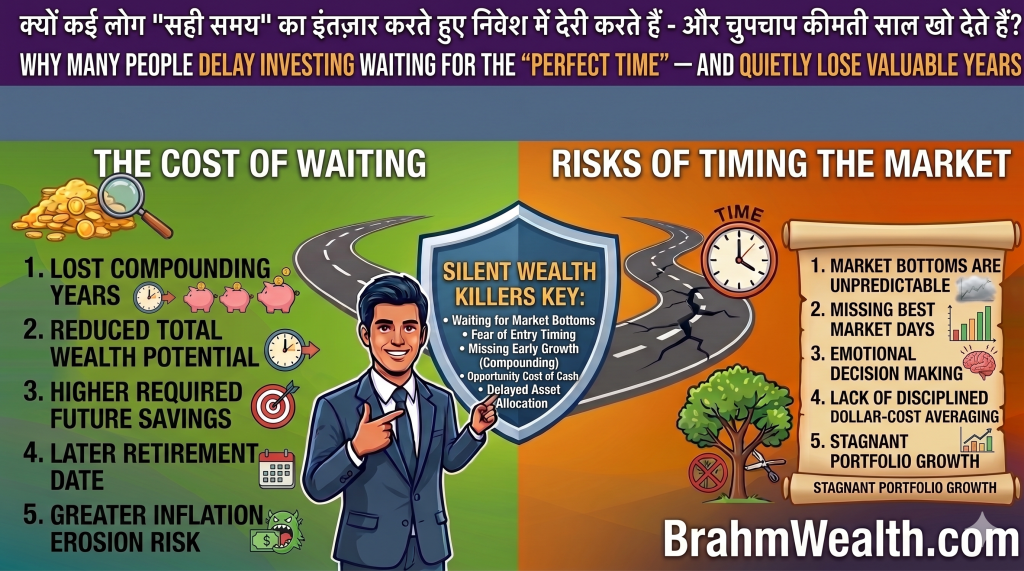

while people wait for the “perfect time,” inflation and lost compounding time quietly continue working against them.

This is one of the biggest hidden reasons why many people struggle to build long-term wealth despite earning reasonably well.

Why People Hesitate to Start Investing

Investing often feels emotionally uncomfortable initially because:

- markets fluctuate,

- returns are uncertain,

- and financial fear feels natural.

Some people fear:

- temporary losses,

- market crashes,

- or making wrong decisions.

Others assume:

successful investing requires perfect timing.

But in reality:

- long-term investing often rewards consistency more than perfection.

Example 1 — Starting Early vs Waiting for “Better Time”

Let’s compare two investors.

Investor A — Starts Early

Assumptions

- SIP = ₹10,000/month

- Expected annual return = 12%

- Investment duration = 25 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹30 lakh |

| Approximate Corpus | ₹1.8–2 crore |

Investor B — Waits 5 Years

Assumptions

- Same SIP amount

- Delays investing by 5 years

- Investment duration = 20 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹24 lakh |

| Approximate Corpus | ₹95 lakh–1 crore |

This demonstrates:

just delaying investing by a few years may potentially reduce long-term compounding power significantly.

Why Time Often Matters More Than Timing

Many beginners focus heavily on:

- finding perfect market entry,

- predicting market crashes,

- or waiting for “safe conditions.”

But long-term investing often depends more on:

- staying invested,

- remaining disciplined,

- and allowing compounding enough time to work.

This is why experienced investors often say:

“Time in the market may potentially matter more than timing the market.”

Why Inflation Makes Delaying Investments Expensive

Inflation silently increases:

- daily expenses,

- healthcare costs,

- education fees,

- travel costs,

- and lifestyle expenses.

Example 2 — Inflation Impact Over Time

Assumptions

- Current monthly household expense = ₹50,000

- Inflation assumption = 6%

- Time horizon = 20 years

Approximate Future Expense

| Today’s Expense | Future Equivalent |

|---|---|

| ₹50,000/month | ₹1.6 lakh/month |

This means:

- future financial goals may potentially become much more expensive over time.

This is why:

delaying investing may quietly increase future financial pressure.

Why SIP Investing Helps Beginners Start

SIP investing became popular because:

- small amounts may be invested gradually,

- emotional timing pressure reduces,

- and investing discipline improves over time.

SIP investing also helps people:

- start investing without needing huge capital initially.

At BrahmWealth.com, the focus is on helping beginners understand practical long-term investing behavior in simple and realistic language.

Example 3 — Small SIP Started Early

Assumptions

- SIP = ₹5,000/month

- Expected annual return = 12%

- Investment duration = 30 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹18 lakh |

| Approximate Corpus | ₹1.5 crore+ |

This demonstrates:

- even moderate SIP amounts,

- combined with long-term consistency,

may potentially create meaningful future wealth.

SIP Future Value Formula

Where:

- M = Future maturity value

- P = Monthly SIP amount

- i = Monthly rate of return

- n = Total number of monthly instalments

This formula helps estimate how regular monthly SIP investments may potentially grow over time through compounding and disciplined long-term investing.

Monthly Rate Formula

i=12×100Annual Return

Where:

- i = Monthly rate of return

Example:

- Annual return = 12%

- Monthly rate = 0.01

Total Number of Months Formula

n=Years×12

Where:

- n = Total number of monthly instalments

Example:

- Investment duration = 20 years

- Total months = 240

Why Many People Still Delay Investing

Common reasons include:

- fear of losses,

- confusion about investing,

- waiting for higher income,

- or belief that small investments are meaningless.

But long-term wealth creation often rewards:

- starting early,

- investing consistently,

- and remaining patient.

Why Emotional Market Timing Often Fails

Many people try to:

- invest only during market crashes,

- avoid all volatility,

- or perfectly predict market movements.

But markets are influenced by:

- global events,

- economic conditions,

- investor emotions,

- and uncertainty.

Consistently predicting markets is extremely difficult.

This is why disciplined long-term investing usually becomes more practical for many investors.

Important Reality Check

All investment examples in this article are educational illustrations based on assumptions.

Actual investment returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Investors should always evaluate:

- financial goals,

- risk tolerance,

- and suitability carefully.

Common Financial Mistakes Many People Make

Many people:

- delay investing repeatedly,

- wait endlessly for perfect timing,

- stop SIPs emotionally,

- or underestimate inflation.

Others assume:

investing can begin “later.”

But long-term compounding often rewards:

- early action,

- patience,

- and consistency.

How Can Someone Start Investing More Practically?

Simple starting steps may include:

- Starting SIPs with manageable amounts

- Thinking long-term financially

- Avoiding emotional market timing

- Increasing SIP gradually with income growth

- Staying disciplined during volatility

Healthy investing behavior usually improves gradually over time.

Final Thoughts

Waiting for the “perfect time” to invest often feels emotionally comfortable.

But over long periods:

- delayed investing,

- lost compounding time,

- and inflation

may potentially reduce wealth creation significantly.

Because:

in long-term investing, starting consistently often becomes more important than starting perfectly.