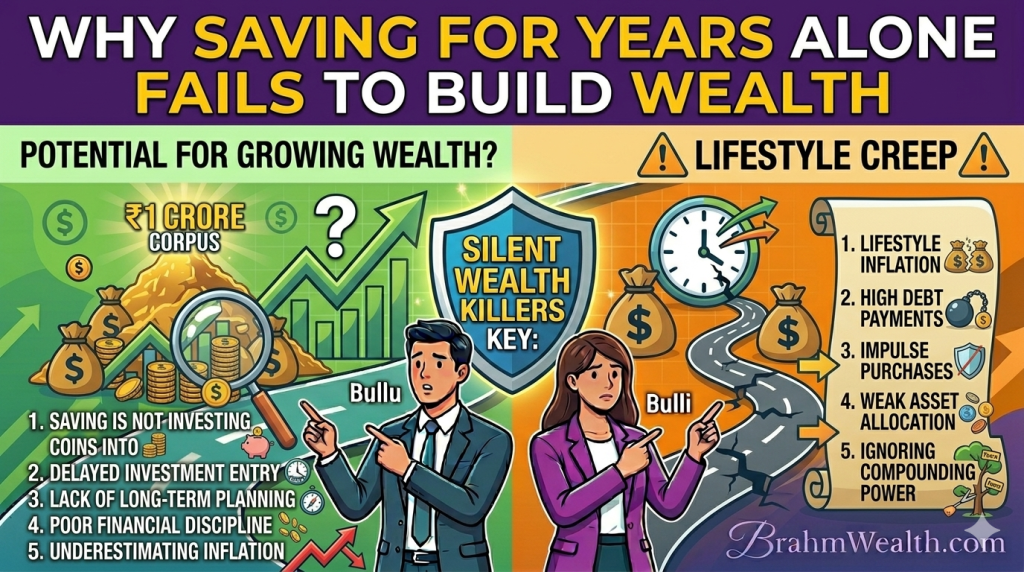

Saving Money and Building Wealth Are Not Always the Same Thing

Narrated by BrahmWealth.com

By Brahm Prakash Rathore — Mutual Fund Distributor ARN359190 | Founder, BrahmWealth

Many people believe:

“I am saving money regularly, so my financial future is secure.”

At first, this sounds sensible.

After all:

- saving money is important,

- financial discipline matters,

- and avoiding unnecessary spending is healthy.

But over long periods:

- saving alone may not always create meaningful wealth,

especially when: - inflation keeps increasing,

- expenses rise,

- and purchasing power gradually decreases.

This is why modern financial awareness increasingly focuses on:

the difference between saving money and growing money.

Why Traditional Saving Alone May Become Insufficient

Earlier generations often depended heavily on:

- savings accounts,

- cash savings,

- recurring deposits,

- or fixed deposits.

At that time:

- expenses were lower,

- inflation impact was lower,

- and financial pressure was simpler.

Today:

- education costs are rising rapidly,

- healthcare expenses are increasing,

- retirement periods are becoming longer,

- and inflation continuously affects purchasing power.

Because of this:

money that remains idle for very long periods may potentially lose real value over time.

Example 1 — Saving vs Investing

Let’s understand this practically.

Person A — Only Saving Money

Assumptions

- Saves ₹10,000 monthly

- Keeps money mostly idle or in very low-growth instruments

- Time horizon = 20 years

Approximate Result

| Details | Amount |

|---|---|

| Total Savings | ₹24 lakh |

| Real Purchasing Power After Inflation | Potentially much lower |

Even though discipline exists:

- long-term growth may remain limited.

Person B — Saving + Investing Systematically

Assumptions

- ₹10,000 monthly SIP

- Expected annual return = 12%

- Investment duration = 20 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹24 lakh |

| Approximate Corpus | ₹95 lakh–1 crore |

This demonstrates:

disciplined investing combined with time and compounding may potentially create significantly stronger long-term wealth growth.

Why Inflation Quietly Reduces Purchasing Power

One of the biggest hidden financial risks is:

inflation.

Inflation means:

- the cost of living gradually rises over time.

For example:

- groceries,

- healthcare,

- school fees,

- fuel,

- and property prices

often become much more expensive over long periods.

Example 2 — Inflation Reality

Assumptions

- Current monthly household expense = ₹60,000

- Inflation assumption = 6%

- Time horizon = 20 years

Approximate Future Expense

| Today’s Expense | Future Equivalent |

|---|---|

| ₹60,000/month | ₹1.9 lakh/month |

This is why:

financial awareness is not only about saving —

but also about protecting future purchasing power.

Why Investing Awareness Is Becoming Essential

Modern financial life is changing rapidly.

Today:

- retirement may last 25–30 years,

- healthcare costs are rising,

- education planning is expensive,

- and financial dependency risks are increasing.

This is why:

- SIP investing,

- long-term planning,

- and compounding awareness

are becoming increasingly important.

At BrahmWealth.com, the goal is to help beginners understand these concepts in simple practical language instead of confusing technical finance jargon.

Why SIP Investing Became Popular

SIP investing became popular because:

- investing becomes systematic,

- discipline improves,

- and small amounts may potentially create meaningful long-term wealth through compounding.

SIP investing also helps reduce:

- emotional investing behavior,

- and market timing pressure.

Example 3 — Small SIP, Large Long-Term Difference

Assumptions

- SIP = ₹5,000/month

- Expected annual return = 12%

- Investment duration = 30 years

Approximate Outcome

| Details | Amount |

|---|---|

| Total Investment | ₹18 lakh |

| Approximate Corpus | ₹1.5 crore+ |

This demonstrates:

- consistency,

- patience,

- and long-term compounding

may potentially create surprisingly powerful wealth outcomes.

How Compounding Supports Wealth Creation

Compounding means:

investment growth may generate additional growth over time.

FV=P×r(1+r)n−1

This is why:

- long-term investing,

- early SIP discipline,

- and patience

often become extremely important in wealth creation.

Why Many People Still Avoid Investing

Common reasons include:

- fear of market fluctuations,

- lack of financial awareness,

- confusion about where to begin,

- or belief that investing requires huge money.

But in reality:

- even small disciplined investing habits

may potentially become meaningful over long periods.

Example 4 — Delaying Investments vs Starting Early

Investor A

- starts ₹8,000 SIP at age 25

- invests for 30 years

Investor B

- delays investing until age 35

- invests same ₹8,000 SIP for 20 years

Approximate Observation

| Investor | Approximate Corpus |

|---|---|

| Investor A | ₹2.5–3 crore |

| Investor B | ₹75 lakh–1 crore |

This demonstrates:

time may quietly become one of the most powerful wealth-building factors.

Financial Awareness Is Not About Taking Extreme Risk

Healthy financial awareness usually focuses on:

- discipline,

- realistic expectations,

- gradual wealth creation,

- and long-term financial stability.

It is not about:

- overnight riches,

- unrealistic profits,

- or reckless financial behavior.

Important Reality Check

All investment examples in this article are educational illustrations based on assumptions.

Actual investment returns:

- fluctuate,

- are market-linked,

- and are never guaranteed.

Investors should always evaluate:

- financial goals,

- risk tolerance,

- and suitability carefully.

Common Financial Mistakes Many People Make

Many people:

- save money but never invest,

- delay investing repeatedly,

- underestimate inflation,

- or spend emotionally after salary increases.

Others assume:

investing can start “later.”

But long-term wealth creation often rewards:

- early action,

- disciplined investing,

- and financial consistency.

How Can Someone Start Building Better Financial Awareness?

Simple starting steps may include:

- Understanding inflation

- Learning basic investing concepts

- Starting small SIP investments

- Building emergency savings gradually

- Thinking long-term financially

Financial awareness usually develops step by step over time.

Final Thoughts

Saving money is important.

But in modern financial life:

- saving alone may not always be enough for long-term wealth creation.

This is why:

- investing awareness,

- disciplined SIP habits,

- and long-term financial planning

may potentially become extremely valuable for future financial security.

Because:

protecting money is important —

but growing money responsibly may become equally important over time.